Florida 4-Point & Wind Mitigation Inspections: How to Save on Homeowners Insurance in Jacksonville

Florida's insurance market is brutal, especially on older homes. The four-point and wind mitigation inspections are two of the highest-ROI services you can buy as a Jacksonville homeowner. Here's exactly how they work and how much they can save.

If you own or are buying an older home in Jacksonville, chances are high that your insurance carrier has already asked for one or both of these: a four-point inspection and a wind mitigation inspection. And if they haven't yet, they probably will at renewal.

These two inspections sound intimidating and expensive. They're actually some of the best money a Florida homeowner can spend. Done right, they can unlock hundreds — sometimes thousands — of dollars in annual insurance savings while keeping your coverage in place. Here's everything you need to know.

The Four-Point Inspection: Insurance Companies' Minimum

Once a home in Florida is 25 years old or more, most insurance carriers will not write or renew a homeowners policy without a four-point inspection. It's their way of making sure the core systems of the home aren't an unmanageable risk.

What "four points" means:

- Roof — age, material, condition, and estimated remaining service life

- Electrical — panel brand, wire type (copper, aluminum, knob-and-tube), grounding, and obvious hazards

- Plumbing — supply lines (copper, PEX, polybutylene, CPVC, galvanized), drains, and water heater age

- HVAC — age, type, and working condition

The inspection itself is quick — usually an hour or less — and the report is filled out on the standard Citizens form that nearly every Florida carrier accepts. I typically deliver it the same day.

What carriers actually care about:

- Roofs older than 15–20 years (especially 3-tab shingles)

- Outdated electrical: aluminum branch wiring, Federal Pacific or Zinsco panels, knob-and-tube

- Plumbing that's known to fail: polybutylene, cast iron drains, galvanized supply

- HVAC systems at or past their useful life (typically 12–18 years)

If your home has any of these, the four-point report tells the carrier — and you can address issues before renewal rather than being surprised by a non-renewal letter.

The Wind Mitigation Inspection: Where the Real Savings Are

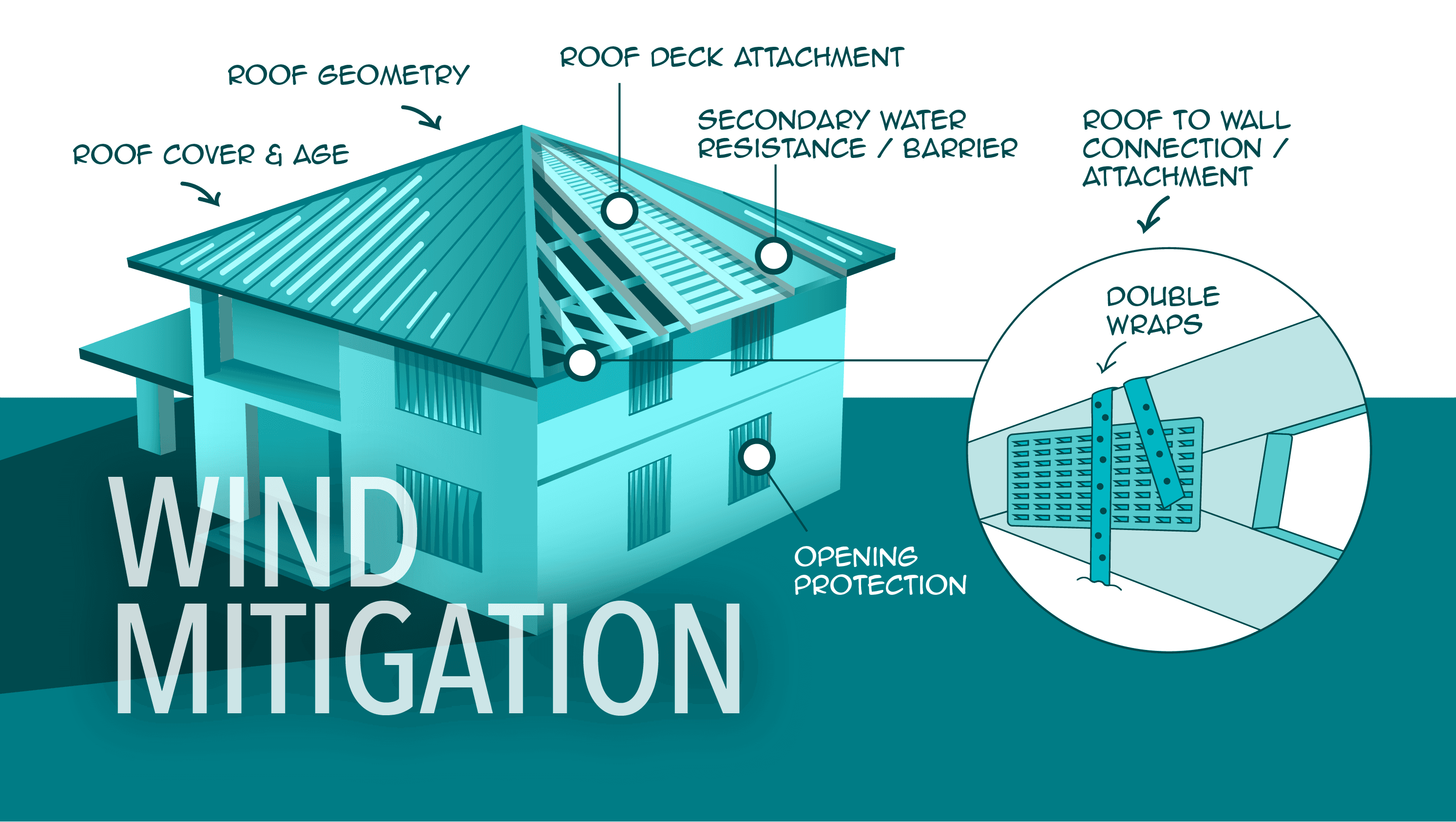

Florida law requires insurance carriers to offer discounts to homeowners whose properties have features that reduce hurricane damage. The wind mitigation inspection — filed on the official OIR-B1-1802 form — documents those features for your carrier.

What we document:

- Year of construction and roof permitting — newer roofs generally mean newer building codes

- Roof covering — is the shingle/tile/metal covering rated and properly installed under FBC (Florida Building Code)?

- Roof deck attachment — how the sheathing is nailed down (nail size, spacing, and type matter)

- Roof-to-wall connection — toe-nails, clips, single wraps, or double wraps?

- Roof geometry — hip roofs earn bigger discounts than gable roofs because they handle wind better

- Secondary water resistance (SWR) — a sealed roof deck that slows water intrusion if shingles blow off

- Opening protection — impact-rated windows and doors, or code-approved shutters

Each feature the home has earns you a discount. Strong homes can qualify for discounts of 20% to 45% on the wind portion of your premium — and the wind portion is often the biggest chunk of a Florida homeowner's bill.

The math that matters: If your annual premium is $3,000 and the wind portion is $1,800, a 30% discount saves you $540 per year. A wind mitigation inspection typically pays for itself in the first month.

Bundle Them and Save Time

Both inspections can be done in a single visit. If you're buying an older home or renewing an aging policy, booking both together saves you a second appointment and a second trip charge. I do this routinely throughout Jacksonville and the surrounding counties.

When to Schedule

- Buying an older home — schedule both before closing so the numbers flow into your new policy

- Before a renewal — if your carrier flagged your home for non-renewal, get both done fast

- After a roof replacement — a new roof usually earns significant wind mitigation credits you won't get automatically

- After window/door upgrades to impact-rated units — opening protection alone can be worth hundreds per year

What You Need to Do

- Have documentation of any roof permits, roof replacement dates, and window/door upgrades ready

- Make sure the attic is accessible so I can verify the roof-to-wall connection

- Have your current insurance declarations page handy so your agent knows exactly what to apply the credits to

Ready to Save on Your Jacksonville Insurance?

Blue Line Inspections LLC performs same-day four-point and wind mitigation inspections throughout Baker, Duval, Clay, Nassau, Columbia, Bradford, Union, St. Johns, Putnam, and Alachua counties. Call or text 904-576-9338 and I'll get you on the schedule.

Jacksonville trusted. Northeast Florida proven.

Your home deserves local expertise.

InterNACHI Certified Inspector serving Jacksonville and the surrounding Northeast Florida counties.